SVB’s collapse explained in 6 steps

.png)

The story of Silicon Valley Bank (SVB) serves as a cautionary tale for other banks, highlighting the dangers of investing too heavily and having insufficient liquidity. In the years 2020 to 2022, SVB received an influx of deposits that they maximized by investing in longer-term securities and loans during the low-interest environment. However, when customer withdrawals and high-interest rates hit them hard, they found themselves with a liquidity crisis. This story covers the fall of SVB illustrated through data.

The data for this article comes from BankRegData, which sources data from the Quarterly Call Reports that each bank is required to report to their Regulator each quarter.

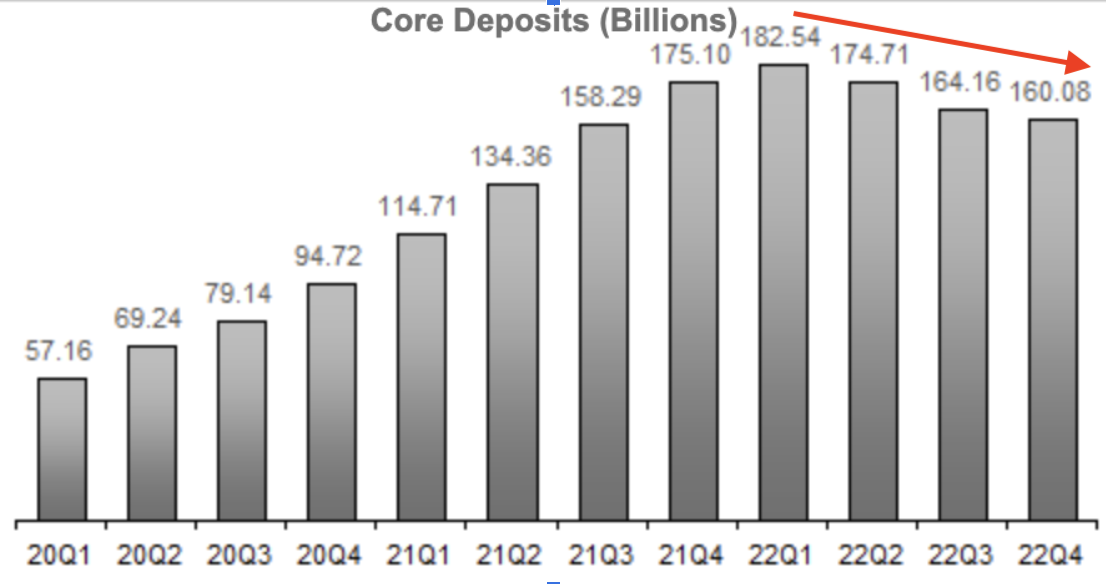

1. Between Quarter 1 2020 and Quarter 1 2022, SVB's deposits increased by $125 billion amid the massive influx of money to VCs investing in startups using SVB.

2. Where did SVB keep those deposits? 56% went to securities, 35% was loaned out to maximize their yield, and 6% remained as cash on hand.

3. Then, as you can see in the first graph SVB had an outflow of deposits from Quarter 1 2022 to Quarter4 2022, with a decrease in $22 billion in deposits which they needed to pay back to customers.

4. Why did this outflow happen? In addition to the change in the VC fundraising climate, as the interest rate increased in 2022, companies could put their money in US treasuries and get a risk-free high yield - where in contrast SVB was giving out .05-1.24% at this time.

During 2021's near zero interest rate environment, SVB locked their money in longer-term securities to garner a higher yield.

5. Because SVB invested the majority of its cash into long-term securities and loans to maximize its yield, they did not have enough cash on hand to pay back these withdrawals. They needed to pay back $22 billion but only had $12.5 billion cash on hand.

Below you can see how SVB borrowed;

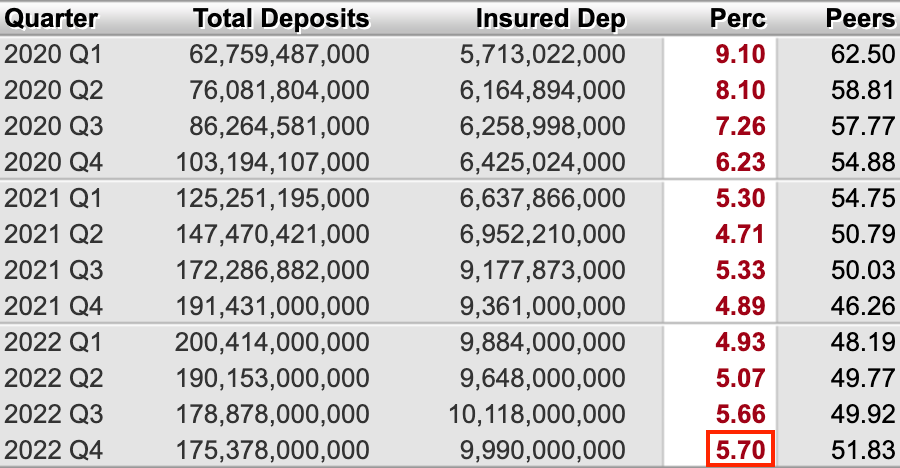

6. SVB's announcement of a $1.75 billion capital raise led to widespread panic, particularly because the vast majority of the funds they held were uninsured, with less than 6% being covered. Ultimately, this led to the downfall of SVB.

Practical Questions to Ask to Ensure Your Bank is Well Managed

- How much liquidity does the bank have on hand to cover unexpected withdrawals or shortfalls?

- What percentage of the bank's deposits are invested in longer-term securities and loans, and what percentage is kept as cash reserves?

- How does the bank diversify its investment portfolio to minimize potential losses and reduce risks?

- How does the bank manage credit risk and ensure the creditworthiness of its borrowers?

- What is the bank's strategy for managing interest rate risk?

- What percent of deposits are insured?

- What measures does the bank have in place to ensure the safety and security of customer deposits?

Special thanks to Bill Moreland from BankRegData

Up to 3,500 bonus and 3% cash-back on all card spend [3], 6 months off payroll, and 50% off bookkeeping for 6 months, free R&D credit.

Frequently Asked Questions

Startup grants are crucial in helping new businesses in West Virginia grow and succeed. They provide financial support without the need for repayment, offering startups a unique opportunity to access resources that can drive innovation and development.

- How can nonprofits in West Virginia apply for state grants?

Startup grants are crucial in helping new businesses in West Virginia grow and succeed. They provide financial support without the need for repayment, offering startups a unique opportunity to access resources that can drive innovation and development.

- What financial aid is offered to startups in West Virginia affected by COVID-19?

Startup grants are crucial in helping new businesses in West Virginia grow and succeed. They provide financial support without the need for repayment, offering startups a unique opportunity to access resources that can drive innovation and development.

- Are there specific grants for innovation or technology-based startups in West Virginia?

Startup grants are crucial in helping new businesses in West Virginia grow and succeed. They provide financial support without the need for repayment, offering startups a unique opportunity to access resources that can drive innovation and development.

- What are the requirements for West Virginia college grants for entrepreneurs?

Startup grants are crucial in helping new businesses in West Virginia grow and succeed. They provide financial support without the need for repayment, offering startups a unique opportunity to access resources that can drive innovation and development.

- How does one apply for housing or home-based business grants in West Virginia?

Startup grants are crucial in helping new businesses in West Virginia grow and succeed. They provide financial support without the need for repayment, offering startups a unique opportunity to access resources that can drive innovation and development.

Practical Questions to Ask to Ensure Your Bank is Well Managed

How much liquidity does the bank have on hand to cover unexpected withdrawals or shortfalls?

What percentage of the bank's deposits are invested in longer-term securities and loans, and what percentage is kept as cash reserves?

How does the bank diversify its investment portfolio to minimize potential losses and reduce risks?

.png)